Time is your ally.

That is one of AMM’s five core principles, and we mean it.

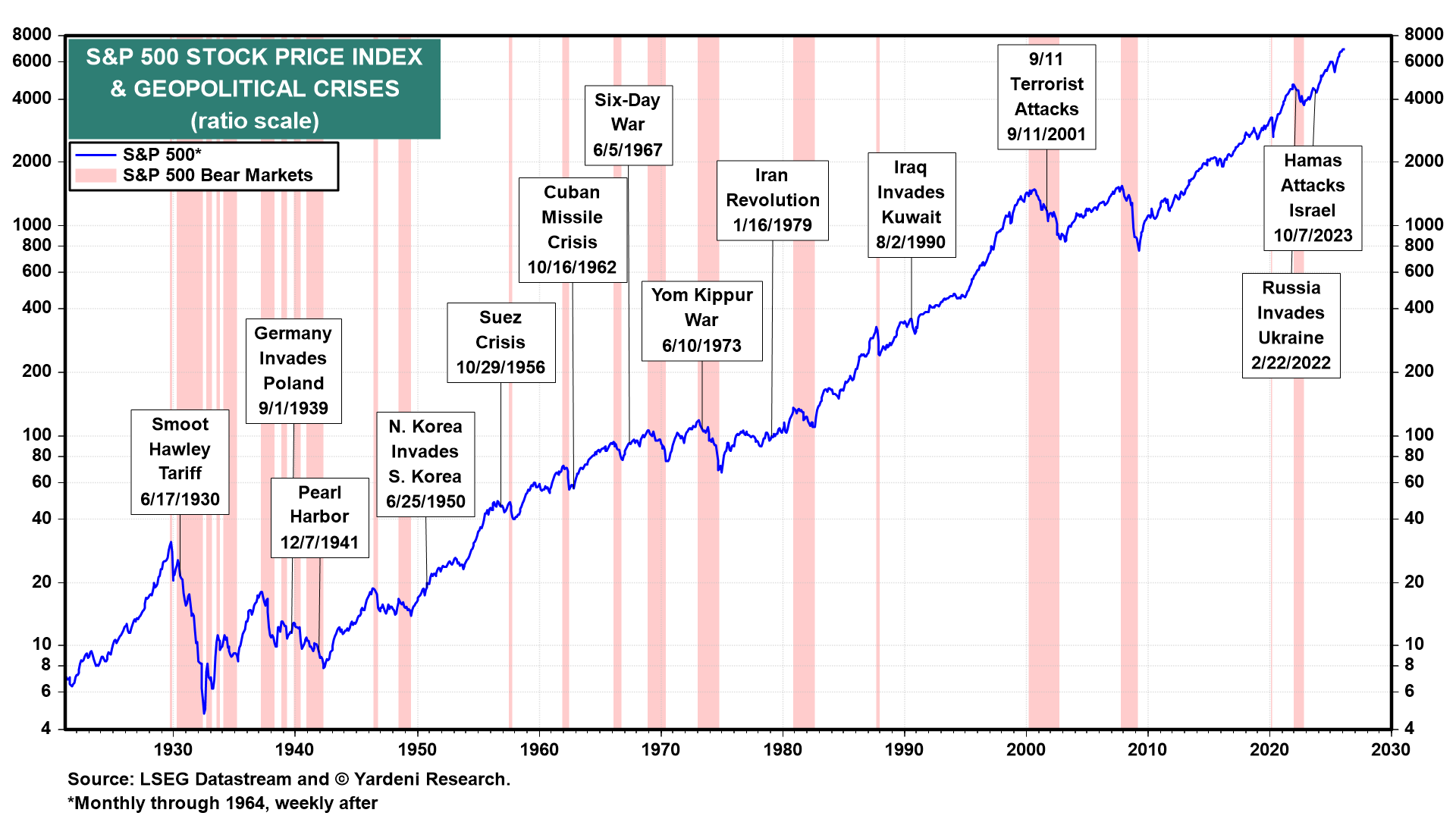

But there is a paradox buried in that statement. The longer you stay invested, the more likely you are to experience events like the recent escalation of conflict in the Middle East — the kind of shock that rattles markets.

A longer time horizon does improve your odds of good outcomes. But it does so precisely because it exposes you to more disruptions along the way. Investors earn a return premium over cash and bonds for holding stocks precisely because they carry this risk. Remove the exposure to short-term discomfort and you remove the long-term return that comes with it.

History is instructive here, though the lesson is more nuanced than “markets always recover.” Looking at two examples from recent decades makes the point.

The Gulf War in 1990 hit during a mid-cycle expansion. Once the initial uncertainty passed, the economy’s underlying momentum took over. The S&P 500 bottomed about three months after the conflict began and gained over 25% in the year that followed. The shock was real — but the economy was healthy enough to absorb it.

September 11th was different. Markets did recover their initial losses within about two months. But that recovery didn’t last. The National Bureau of Economic Research (NBER) had already dated the start of the recession to March 2001 — months before the attacks. The shock didn’t cause the bear market. It deepened one that was already underway.

The current environment looks more like the former than the latter. Heading into the recent conflict, the U.S. economy was in expansion — labor markets were solid, earnings were broadly positive, and credit was not under stress. That doesn’t guarantee a quick resolution in markets, but it’s a better starting point than a shock that lands in a weakening economy. Our base case is that the expansion reasserts itself once the immediate uncertainty settles.

That said, we don’t want to be dismissive of the risks. This particular conflict has the potential to disrupt the global energy supply. A sustained disruption to oil flows through the Strait of Hormuz — through which it is estimated roughly 20% of global petroleum passes — could push energy prices meaningfully higher, complicate the Fed’s inflation fight, and in a worst-case scenario, tip the economy toward recession. We don’t think that’s the most likely outcome. But it’s a real scenario, and one that diversified portfolios are better positioned to handle than concentrated ones.

So, what should you actually do? Not all short-term thinking is wrong. There are legitimate reasons to revisit your allocation: a near-term need for funds, a real change in your time horizon or risk tolerance, a life event that shifts the picture. Those conversations are worth having.

However, making changes to a well-conceived investment strategy due solely to fear of further declines, or the belief that you can time when to get back in is imprudent and likely wealth destructive. The evidence on market timing is pretty clear — it doesn’t work reliably. And missing even a handful of the market’s best days can do real damage to long-term returns.

According to research from Hartford Funds, an investor who stayed fully invested in the S&P 500 from 1994 to 2025 would have earned more than twice as much one who missed just the 10 best days over that period. What makes that statistic particularly striking is where those best days tend to occur. 76% of the market’s best days happened either during a bear market or in the first two months of a bull market recovery — exactly when investors are most tempted to be out of the market.

To be fair, the math works in the other direction too. Miss the 10 worst days and your returns likely improve meaningfully as well. But here is the problem with that line of thinking: no one rings a bell at the top or the bottom. The best and worst days are often separated by days or even hours, and the research consistently shows that investors who try to dodge the bad days end up missing the good ones too. Trying to step out when things look bad and back in when they look better is a strategy that sounds sensible but rarely works in practice.

So, if market timing isn’t the answer, what is? In our view, the better approach to managing risk and return over the long run is to build a portfolio that doesn’t require you to make those calls in the first place. That means genuine diversification — across asset classes, geographies, and market capitalizations — and paying attention to portfolio duration.

Duration is just a way of thinking about time horizon at the asset level — matching how long each investment needs to work to the specific need it is meant to serve. And just as individual assets carry their own duration, the portfolio as a whole has a blended duration — a reflection of how the short, intermediate, and long-term assets combine to align with your overall investment horizon and liquidity needs.

We want to be clear that this doesn’t mean holding all assets all of the time. As active managers, we make deliberate decisions about where to invest and where not to. There are times when we underweight or avoid certain asset classes entirely based on valuation, risk, or opportunity.

But the framework is built around diversification as a principle — ensuring that no single bet defines the outcome, and that the portfolio can weather different environments without requiring perfect foresight. Not every dollar in your portfolio needs to work on a 20+-year time horizon. Stocks are long-duration assets by nature, and they should be held with that in mind. But shorter-term bonds, Treasuries, and cash serve a different purpose. They provide income and stability when equities are under pressure. The goal is to match the duration of each asset to the need it is meant to serve — so that short-term market volatility doesn’t impair your long-term investment strategy.

Time is your ally. But it works best when your portfolio is built for your specific objectives, risk tolerance and time frame.

Year-to-Date Performance Review

Q1 was a good reminder of why diversification matters. Large-cap U.S. stocks gave back some ground, while mid-cap, small-cap, and emerging market stocks all posted positive returns. International developed markets also held their ground. Gold was a standout, and money market funds continued to offer relatively attractive yields. The broad bond market was essentially flat.

| Asset Class | Index / ETF | YTD Return |

| Large-Cap U.S. Stocks | S&P 500 | -4.3% |

| Mid-Cap U.S. Stocks | S&P 400 | +2.5% |

| Small-Cap U.S. Stocks | S&P 600 | +3.5% |

| International Stocks | EFA | +1.0% |

| Emerging Market Stocks | EEM | +2.79% |

| Bonds | AGG | +.05% |

| Gold | — | +5.5% |

| Money Market | — | ~3.5% yield |

Returns are year-to-date through March 31, 2026.

Current Outlook*

U.S. Stocks

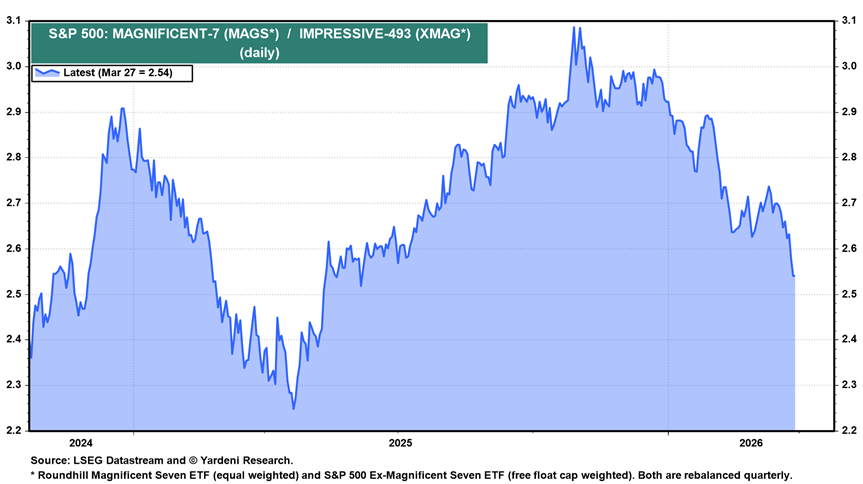

U.S. stocks had three strong years heading into 2025, but a large portion of those gains came from a narrow group of mega-cap technology companies. Collectively referred to as the Magnificent 7 (Mag-7), these companies drove an outsized share of index returns, which left diversified investors — those with exposure to mid-cap, small-cap, and value-oriented sectors — feeling like they were leaving something on the table.

That has started to change. Over roughly the past nine months, the S&P 493 — the S&P 500 index minus the Magnificent 7 — has outperformed the headline index with increasing consistency. The mid- and small-cap returns in the Q1 table above are a good example of this broadening. For AMM asset allocation portfolios, which have maintained diversification across market caps and with a tilt toward value, this is a welcome shift.

The underlying earnings picture supports this view. Q4 2025 was one of the strongest earnings seasons on record. The S&P 500 posted blended year-over-year earnings growth of approximately 13.5% — the tenth consecutive quarter of positive growth. According to Yardeni Research, ten of eleven sectors delivered rising earnings, and the S&P 493 hit a record-high earnings quarter, beating earnings estimates by 5.7%. That earnings beat actually exceeded the Magnificent 7’s 5.4% earnings surprise rate. Looking ahead, Q1 2026 consensus earnings growth is tracking around 12.9% — a figure that has held up well despite the recent Middle East disruption. Revenue growth is expected across nearly all eleven sectors, with Information Technology still leading at an estimated 27% year-over-year. The earnings backdrop remains solid.

International Stocks

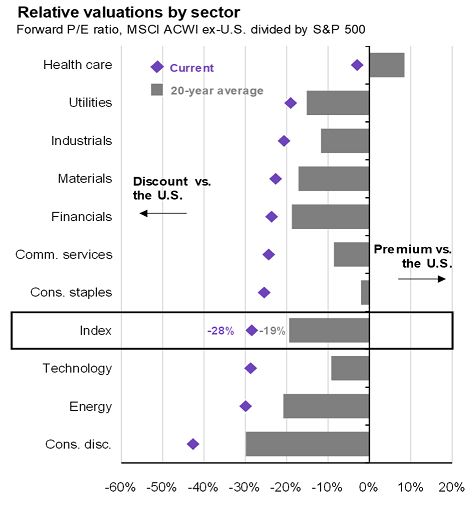

The same logic that drives our small/mid-cap and value exposure applies here. Staying diversified across geographies means you will sometimes trail a concentrated domestic strategy — and sometimes benefit when the cycle turns. Right now, it appears to be turning. The valuation case is compelling too.

The ACWI — the MSCI All Country World Index, which tracks stocks across both developed and emerging markets globally — provides a useful lens for comparing international valuations to the U.S. Nine of ten sectors in the ACWI ex-U.S. have historically traded at a discount to their U.S. counterparts. That discount has historically averaged around 19%. It now stands at 28%. Valuation alone doesn’t tell you when the gap closes, but it does tell you what you are paying — and right now, international stocks are offering a meaningful discount relative to U.S. stocks. We maintain exposure to both developed and emerging international markets in our asset allocation portfolios.

Source: JP Morgan

Fixed Income

Fixed income serves two purposes: income generation and portfolio stability. Longer-term treasury securities have historically been the best “flight to safety” hedge — they tend to rally when stocks fall. We still believe in that long-run relationship. But the current inflation environment complicates it.

The Fed’s March Summary of Economic Projections revised headline PCE inflation up to 2.7% (from 2.4%) and core PCE to 2.7% (from 2.5%). The path back to the Fed’s 2% inflation target remains uneven, and the Middle East conflict adds potential upside risk to energy prices. In that environment, longer-duration bonds carry real price risk — if inflation stays elevated or the Fed holds rates higher for longer, the “flight to safety” hedge of owning longer duration bonds can work against you.

For this reason, we continue to favor shorter-duration, investment-grade fixed income. We also maintain exposure to TIPS (Treasury Inflation Protected Securities), which provide a hedge if inflation proves stickier than expected. On high yield (below investment grade credit), we continue to avoid it. Credit spreads, a comparative measure of additional return received for additional risk taken, remain historically tight and have not widened significantly in response to the current macro risks — in our view, the market is not offering adequate compensation for that risk.

*Individual accounts will vary based on a client’s stated investment objectives, risk tolerance and time frame. We manage several different strategies, so not every client has exposure to the securities, asset classes or strategies described above. In addition to growth and/or income-oriented asset allocation strategies, we also manage more concentrated equity portfolios that generally carry a higher degree of risk and volatility.

Should you have any questions regarding your investment account(s) and personal financial plans, or if there have been any recent changes to your investment and/or retirement objectives, please contact our office. We can also provide you with a current copy of our SEC form ADV Part 2, at your request.

As always, we thank you for entrusting AMM to help you achieve your investment and retirement objectives.

Best regards,

Your Portfolio Management Team