This past quarter offered another stark reminder of just how difficult it is to outguess markets in the short run. In April, global equities sold off sharply following the surprise announcement of sweeping new tariffs on imported goods — dubbed “Liberation Day” by policymakers, but met with anxiety by investors. While the selloff was swift, the recovery was equally impressive. By late June, the S&P 500 had fully recouped its losses and returned to new highs.

Events like this are unsettling. They test patience and tempt investors to act — to raise cash, to shift allocations, or to “wait for clarity.” But clarity is a luxury rarely afforded in real time. What feels like a turning point in the moment often proves insignificant in hindsight.

Events like this are unsettling. They test patience and tempt investors to act — to raise cash, to shift allocations, or to “wait for clarity.” But clarity is a luxury rarely afforded in real time. What feels like a turning point in the moment often proves insignificant in hindsight.

And these episodes are far more common than most investors realize. Economist Ed Yardeni has tracked 72 distinct “panic attacks” in the market since 2009 — each one accompanied by headlines, volatility, and an urgent sense that “this time is different.” Most of these have since faded into the background, quickly replaced by new concerns.

Rather than trying to anticipate each twist and turn, we focus on building portfolios that can endure a variety of outcomes. That’s where discipline comes in. But what exactly does discipline mean in an investment context?

Discipline Means Having a Framework

Discipline is not about doing nothing. It’s about doing the right things — consistently, and with purpose — even when headlines and emotions pull us in other directions. At AMM, our investment discipline is grounded in several core principles:

Asset Allocation

We begin with the most important decision: how to allocate capital across stocks, bonds, and other assets based on our clients’ goals, time horizon, and risk tolerance. This strategic mix is designed not for this quarter or this year, but for the next 10, 20, or 30 years. Proper asset allocation allows portfolios to participate in market upside while helping to buffer volatility.

Diversification

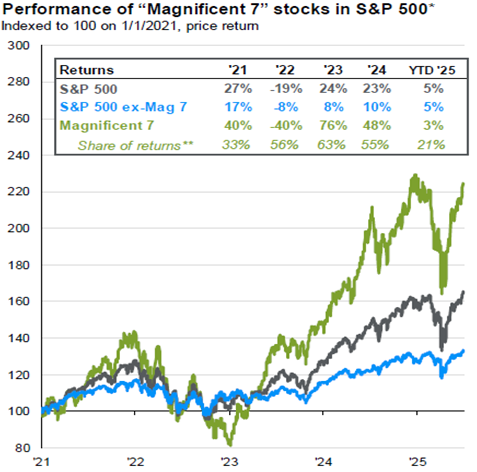

When a small group of companies is driving most of the market’s return — as we’ve seen in recent years with the so-called “Magnificent Seven” (Apple, Microsoft, Nvidia, Alphabet, Amazon, Meta, and Tesla) — diversification can feel like a drag. These mega-cap technology and consumer names have collectively powered much of the S&P 500’s gains, particularly since the post-COVID rebound. When they’re soaring, portfolios with broader exposure may lag the headline index.

Source: FactSet, Standard & Poor’s, J.P. Morgan Asset Management

It can be uncomfortable to hold investments that aren’t keeping pace with the market leaders — and at times, it may even feel like you’re doing something wrong. That discomfort often leads to second-guessing or the temptation to chase what’s recently worked. But in reality, it’s a feature, not a flaw. Diversification works precisely because it involves owning a mix of assets that behave differently. It reduces reliance on any single company, sector, or theme, and helps ensure portfolios remain resilient across a wide range of economic and market conditions.

At the same time, diversification can be taken too far. Owning a little bit of everything can dilute the impact of good decisions and result in a portfolio that behaves like a benchmark without intention or purpose. We don’t believe in owning every asset under the sun. Instead, we aim to build portfolios that are diversified across complementary sources of return — different asset classes, sectors, and styles that respond differently to various economic environments.

Long-Term Orientation

Investing is often compared to gambling — we hear terms like “playing the market,” “placing a bet,” or “rolling the dice.” It’s not hard to see why. Markets move unpredictably in the short run, headlines are breathless, and outcomes can feel driven by luck.

But in reality, the stock market is the opposite of a casino. In a casino, the longer you play, the more likely you are to lose — because the odds are mathematically stacked against you. With investing, the longer you stay invested, the better your odds get. Time is your greatest ally, not your enemy.

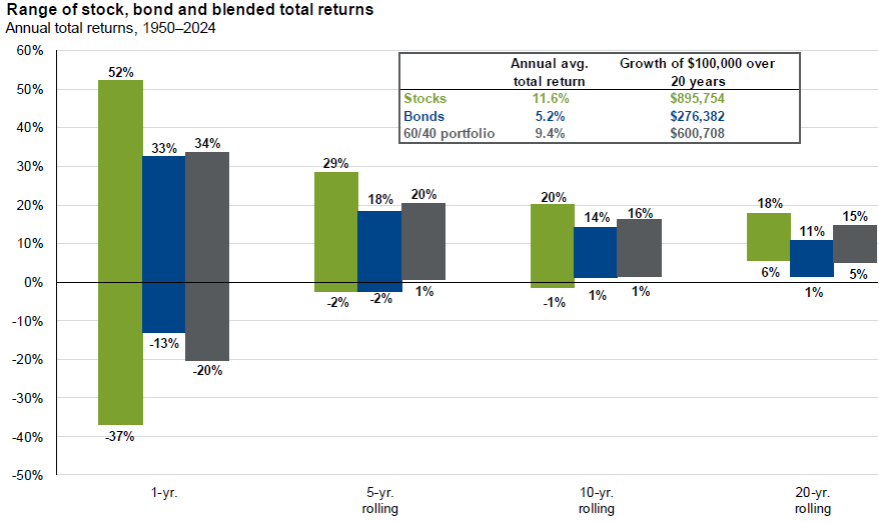

That’s not just philosophy — it’s data-backed. As shown in the chart below, stock returns over one-year periods are highly volatile. But over rolling 10- and 20-year periods, the range of outcomes narrows dramatically, and the likelihood of a positive return increases significantly. The longer your time horizon, the more investing becomes a game of patience and probability — not prediction.

This is why we encourage clients to focus not on where the market will be next quarter, but where it’s likely to be in the years and decades ahead. Markets will always offer reasons for worry. But time, discipline, and diversification turn uncertainty into opportunity.

Source: Bloomberg, FactSet, Federal Reserve, Standard & Poor’s, Strategas/Ibbotson, J.P. Morgan Asset Management

Valuation Awareness

Everyone wants to buy a dollar for fifty cents — and occasionally, markets provide those kinds of opportunities. But most of the time, markets are reasonably efficient. Stocks tend to trade at prices that reflect a wide range of known information, and deep discounts are rare, especially for high-quality businesses.

That’s why being valuation-aware isn’t about always seeking “cheap” — it’s about anchoring our expectations and managing risk. When we pay too high a price for even a great company, the investment becomes fragile. The margin for error shrinks. Future returns may disappoint, not because the business faltered, but because expectations were too high from the start. Conversely, a fair or even modestly undervalued price provides room for resilience. It lowers the bar for a good outcome, and creates asymmetry — more upside potential relative to downside risk.

Valuation is not a precise science, and it doesn’t work on a predictable timeline. But it provides a vital framework for gauging what we’re getting for the price we’re paying. It keeps us grounded — especially when enthusiasm or fear dominates investor sentiment.

Bottom line: discipline is hard. It requires patience when others are acting impulsively, and confidence when others are uncertain. But over time, we believe this kind of deliberate approach is what separates successful long-term investors from short-term speculators.

Year-to-Date Performance and Current Outlook

As of June 30, 2025, most major asset classes posted year-to-date gains:

- Large-Cap U.S. Stocks (S&P 500): +6.20%

- Mid-Cap U.S. Stocks (S&P 400): +.20%

- Small-Cap U.S. Stocks (S&P 600): -4.46%

- Developed International Stocks (MSCI EAFE): +19.45%

- Emerging Market Stocks (MSCI EM): +15.29%

- U.S. Bonds (Bloomberg U.S. Aggregate Index): 4.02%

- Cash / T-Bills (1-Year): ~4% yield

Economic & Market Outlook

Following a sharp drawdown earlier in the year, markets staged an impressive rebound in the second quarter. The S&P 500 rose 5.4% in the first half of 2025, ending June at record highs and marking the fastest recovery on record following a 15% or greater decline. Historical trends also favor continued strength. According to a report from JP Morgan Private Bank, in the 11 prior instances since 2000 where the S&P 500 rose at least 5% in the first half of the year, the index went on to rally further in the second half every time — with full-year returns averaging over 19%.

The U.S. economy continues to defy expectations. Despite tighter financial conditions and a Federal Reserve that remains cautious, growth has remained steady. Labor markets are healthy, consumer spending is resilient, and business investment has picked up in areas such as manufacturing and data infrastructure.

Coming into 2025, markets were pricing in 4–5 rate cuts by the Fed. As inflation has proven stickier than expected, those expectations have been dialed back to one or two cuts, or potentially none at all this year. The Fed’s recent communications have reinforced its desire to see clearer evidence that inflation is on a sustainable path back to 2% before loosening policy.

This shifting backdrop can be frustrating for those trying to position portfolios around near-term policy moves. But for long-term investors, it’s worth noting that the economy is showing strength not because of Fed stimulus, but in spite of higher rates. That’s a sign of underlying economic resilience — not fragility.

U.S. Stocks

Large-cap U.S. stocks continue to make up the core equity exposure in most client portfolios, and for good reason. Many of the world’s most dominant and innovative companies are based in the U.S., particularly in the technology and healthcare sectors. Compared to most other developed economies, the U.S. also benefits from stronger profit margins, a more dynamic private sector, and relatively favorable demographic and productivity trends. These qualitative strengths support long-term confidence in U.S. equities as a foundational portfolio holding.

That said, we are tempering expectations for future returns, where valuations now reflect a great deal of optimism. While the long-term case for U.S. equities remains strong, fully valued shares may lead to more muted gains from current levels — especially if economic or earnings growth slows from its current pace.

In most of our diversified asset allocation portfolios, we continue to maintain exposure to small- and mid-cap stocks. These segments of the market currently trade at valuation discounts relative to large caps, offering higher long-term return potential. While smaller companies may be more sensitive to near-term economic shifts, their lower starting valuations and stronger earnings growth profiles provide an attractive opportunity for patient investors.

International Stocks

International equities — both developed and emerging — have delivered a strong start to the year. But behind those headline returns, the fundamental backdrop remains mixed. In Europe, economic growth continues to underwhelm. The region faces persistent structural headwinds including weak productivity, demographic pressures, and energy challenges. Meanwhile, China is struggling to revive consumer demand and manage a prolonged deflationary property downturn — both of which weigh heavily on investor confidence. Adding to the uncertainty are ongoing global trade tensions, including the potential for new tariffs that could further disrupt supply chains and dampen cross-border investment.

Valuations in both developed and emerging markets remain notably lower than in the U.S., but we believe this discount is largely justified by current fundamentals. Lower relative earnings growth, higher political and regulatory risk, and slower innovation cycles help explain the persistent valuation gap.

That said, there are still reasons to maintain exposure — particularly in select emerging markets. A weaker U.S. dollar, stronger commodity demand, and localized technological innovation have helped support returns in some EM regions. From a portfolio construction standpoint, international stocks also provide useful diversification benefits, especially when U.S. equity valuations are elevated.

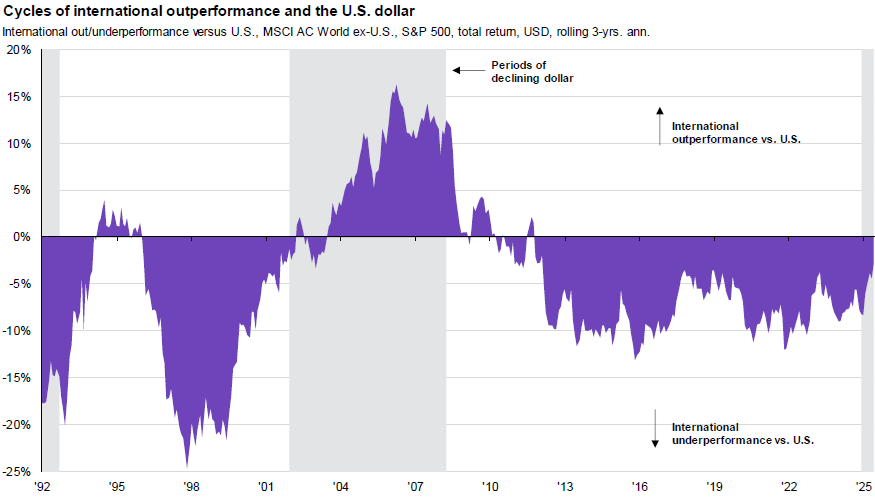

Historical data reminds us that international markets have gone through long cycles of outperformance relative to U.S. equities. While we may eventually enter one of those periods again, we believe it’s still too early to make a high-conviction shift in that direction. For now, we maintain a measured underweight to international equities in asset allocation oriented portfolios.

Source: FactSet, MSCI, Standard & Poor’s, J.P. Morgan Asset Management

Fixed Income

For most clients, the role of fixed income in the portfolio is clear: it serves as a source of stability and ballast, particularly during periods of equity market volatility. To meet that objective, we continue to emphasize high-quality bonds with short to intermediate term durations — including U.S. Treasuries, municipal bonds, and investment-grade corporate debt.

This positioning reflects both current market conditions and our broader philosophy. While the economy remains resilient, spreads on high-yield bonds — the premium investors earn over Treasuries for taking credit risk — remain historically narrow. As shown in the accompanying chart, investors are being paid relatively little extra to take on significantly more risk. As a result, we have maintained limited exposure to that segment of the market.

For qualified investors seeking additional income, we may recommend private income investments, particularly funds backed by real estate collateral. These vehicles can offer attractive yields and modest correlation to public markets, but they come with trade-offs in liquidity and complexity — which is why we evaluate them case by case, with careful due diligence.

Conclusion

While markets will continue to shift and headlines will come and go, our focus remains steady: building resilient portfolios, grounded in long-term discipline, and aligned with your personal goals. We appreciate the opportunity to help guide your financial journey through all phases of the market cycle.

If you have any questions about your investment accounts or personal financial plans—or if there have been any recent changes to your investment or retirement objectives—please reach out. We can also provide a current copy of our ADV Part 2 upon request.

As always, thank you for entrusting AMM to help you achieve your investment and retirement goals.