“Rule number one: most things will prove to be cyclical. Rule number 2: some of the greatest opportunities for gain and loss come when other people forget rule number one.”

Howard Marks

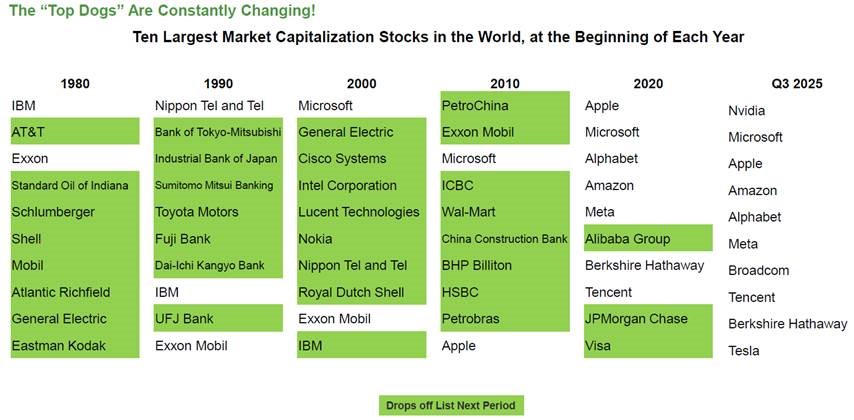

At the start of 1980, the list of the largest companies in the world was dominated by oil and commodity producers—names like Exxon, Mobil, and Royal Dutch Shell—reflecting the previous decade marked by an era of inflation and resource scarcity. By 1990, only one of the companies from the 1980 list remained. Japanese firms now filled the ranks of the world’s largest, capturing nearly half of global market capitalization as investors came to believe Japan’s economic model would dominate the next century. A decade later, at the height of the dot-com boom, only one Japanese stock remained. The new list was dominated by names leveraged to the internet boom—Cisco, Intel, Nokia, and AOL.

By the 2000s, the internet boom gave way to a bust. Leadership shifted again, this time to value-oriented and non-U.S. stocks. China’s acceptance into the World Trade Organization in 2001 ushered in a surge of global trade, infrastructure demand, and commodity strength. By the end of the 2010s, the world’s largest companies included several commodity producers and Chinese banks—symbols of the now-prevailing “China boom.”

Investment trends are cyclical. Whether driven by genuine innovation (Internet – 1990s, AI – 2020s) or a fundamental shift in geo-political power (Japan – 1980s, China – 2000s), a nascent investment trend begins with little fan-fare, going unnoticed by all but a few. Eventually, investors begin to accept the prevailing narrative driving prices higher. Supported by real fundamentals, this phase ushers in mainstream adoption driving prices even higher. Higher prices attract ever more adoption. Eventually, everybody gets it – and that’s when risk is highest.

This is the point when a powerful trend can evolve into a bubble. Bubbles are defined not simply by high prices, but by a collective belief that “this time is different.” They are fueled by a mix of truth and exaggeration — a kernel of real innovation surrounded by layers of speculative enthusiasm. The internet in 1999, housing in 2006, and perhaps artificial intelligence today, all share this mix. There are valid, transformational changes occurring, but markets tend to overshoot the pace and scope of those changes in the short run.

It’s worth remembering that being on trend is essential to long-term success. Innovation and productivity growth are the engines of economic progress, and investors should participate in those themes. But the danger lies in conflating a great company or technology with a great investment at any price.

Is the AI Boom a Bubble?

The question of whether we’re experiencing an AI-driven market bubble has become one of the defining debates of 2025. As we evaluate the evidence, compelling arguments exist on both sides.

But first it is important to note the extreme difficulty of predicting a market bubble. Then Fed Chair Alan Greenspan famously used the term “irrational exuberance” in December 1996 as a warning that the stock market might be overvalued. This was more than 3 years prior to the market top in March of 2000. The Nasdaq went on to gain more than 250% from 1996 to the peak in 2000.

Stanley Druckenmiller, one of the most successful portfolio managers in history, famously shorted the tech bubble in the late 1990s — correctly identifying its excesses — but then reversed course and bought aggressively near the top in 2000, believing he was missing out on further gains. The result was one of his largest career losses. His experience is a timeless reminder that recognizing a bubble is not the same as timing its end.

So we present the below “for and against” Bubble case with humility. Our goal is not to call a bubble top, but to highlight the current risk reward dynamics of THE dominant global investment theme of today.

The Case for a Bubble Concerns

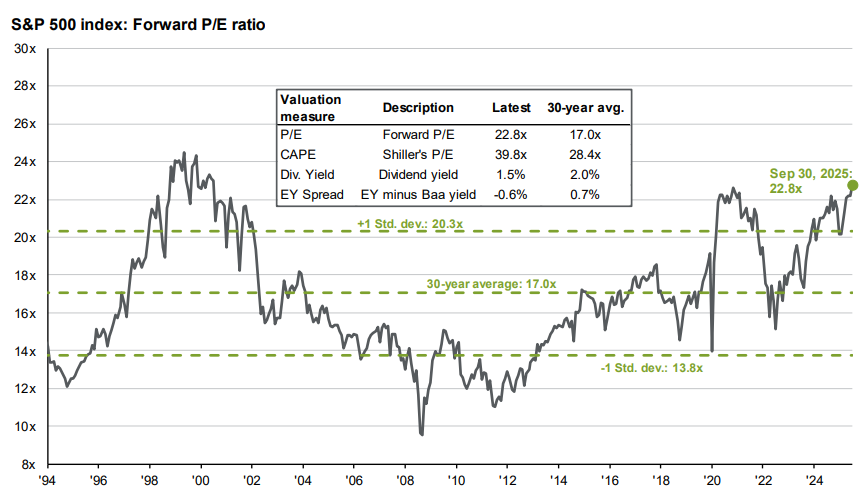

Elevated Valuations

The S&P 500’s forward P/E ratio reached 22.8 at the end of September, uncomfortably close to the 25.0 peak of the 1999 tech bubble.

Source: Bloomberg, FactSet, Moody’s, Refinitiv DataStream, Robert Shiller, Standard & Poor’s, J.P. Morgan Asset Management

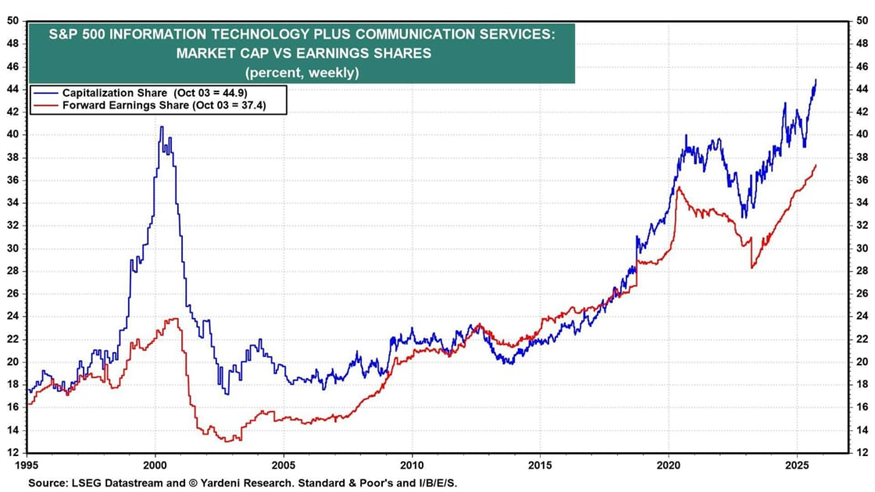

Narrow Market Leadership

The Information Technology and Communication Services sectors now account for a record 44.9% of the S&P 500’s market capitalization—exceeding the 40.7% peak seen during the dot-com era.

Rising Leverage and Speculative Activity

Margin debt surpassed $1 trillion for the first time on record, increasing market sensitivity to sentiment shifts. Leverage amplifies both upside momentum and downside risk.

AI Investment Boom Raises Sustainability Questions

Hyperscalers’ — the massive technology firms that build and operate global cloud computing infrastructure — are investing heavily in AI data centers. These companies, including Amazon, Alphabet, Meta and Microsoft are committing massive sums to data centers and computing infrastructure, driving capital spending to unprecedented levels. Critics warn of “circular” financing loops—where chipmakers and cloud providers fund each other’s expansion—and fear that capacity may be expanding too quickly, echoing the telecom overbuild of the late 1990s.

The Case Against Bubble Fears

Earnings-Driven Valuations

According to data from Yardeni Research, S&P 500 forward earnings per share reached a record in late October, reflecting 9–10% year-over-year growth. Technology leaders now represent 37.4% of the S&P 500’s forward earnings, far above the 23.8% share during the 1999 tech bubble.

Stronger Corporate Balance Sheets

The financing backdrop is fundamentally healthier. A large portion of AI-related capital investment is funded through the strong cash flows of profitable hyperscalers, not through speculative debt issuance.

Credit Market Show Little Sign of Stress

Corporate bond markets remain calm, with high-yield spreads hovering near cycle lows. This suggests that lenders and investors see limited near-term default risk and that financial conditions remain supportive.

A Fundamentally Strong Economy

The U.S. economy has now gone 16 years without a major recession. Productivity gains, tight labor markets, and robust corporate balance sheets have supported growth even amid higher rates.

The Bottom Line

The truth likely lies somewhere in between. We’re witnessing elevated valuations and speculative excess in pockets of the market, but these rest on a foundation of genuine technological transformation and strong corporate fundamentals. Rather than an “everything bubble” destined for catastrophic collapse, we may be experiencing a more sustainable bull market with periodic corrections that create opportunities rather than calamities.

While all bubbles expand on hope, they ultimately burst when the gap between market prices and underlying fundamentals becomes too wide to sustain. High valuation multiples alone don’t necessarily signal a bubble—strong earnings growth can support elevated prices for a time. So far, today’s market levels, though rich, remain anchored to solid fundamentals and earnings growth. The key question for investors is whether those earnings can continue to grow fast enough to sustain current valuations.

How to navigate a frothy or potentially bubbly environment?

The answer lies in discipline rather than prediction. A focus on valuation, quality, and time horizon, are all embedded in AMMs core investment principles. Diversification ensures that participation in innovation doesn’t depend on perfect timing. Patience ensures that when optimism fades, your portfolio remains anchored to enduring fundamentals.

How to navigate a frothy market:

- Acknowledge the Trend, but Don’t Worship It. Structural innovations — like AI today — can reshape industries and drive lasting gains. Participate selectively, but resist the temptation to make large concentrated bets based solely on momentum or narrative strength.

- Respect Valuation. Great companies can be poor investments when purchased at extreme prices. Expanding valuations magnify downside risk if expectations slip, even slightly.

- Favor Quality and Cash Flow. When capital is abundant, weak business models can masquerade as strong ones. Prioritize firms with proven profitability, durable competitive advantages, and the ability to fund growth internally.

- Diversify Across Cycles. Not all sectors or regions move in tandem. Maintaining exposure to a range of assets — including those out of favor — provides balance when leadership inevitably rotates.

- Lean Against Excess, Gradually. Trim or rebalance incrementally when valuations stretch beyond historical norms. Avoid all-or-nothing calls — bubbles can persist longer than expected.

- Stay Time-Disciplined, Not Market-Timed. Anchoring investment decisions to long-term goals, rather than short-term sentiment, prevents behavioral mistakes when euphoria turns to fear.

Year-to-Date Performance and Current Outlook*

As of September 30, 2025, most major asset classes posted year-to-date gains:

- Large-Cap U.S. Stocks (S&P 500): +14.8%

- Mid-Cap U.S. Stocks (S&P 400): +6.1%

- Small-Cap U.S. Stocks (S&P 600): +4.2%

- Developed International Stocks (MSCI EAFE): +25.1%

- Emerging Market Stocks (MSCI EM): +27.5%

- U.S. Bonds (Bloomberg U.S. Aggregate Index): +6.1%

- Cash / T-Bills (1-Year): ≈3.75% yield

Economic & Market Outlook

After a strong first half, markets continued to advance through the third quarter, though with increased volatility as investors weighed mixed economic signals and shifting expectations for Federal Reserve policy. The S&P 500 has gained roughly 10% year-to-date through September, supported by robust corporate earnings, easing inflation pressures, and continued enthusiasm for artificial intelligence and data-infrastructure spending.

The U.S. economy remains remarkably resilient. Growth has moderated from last year’s rapid pace but continues to run above long-term trend levels. Labor markets are steady, household balance sheets remain healthy, and business investment—particularly in manufacturing, technology, and energy infrastructure—has held up well. While consumers are showing signs of fatigue at the lower end of the income spectrum, overall demand continues to support steady output and profits.

Inflation has cooled meaningfully from its 2022 highs, but progress has slowed in recent months. Core measures of inflation remain above the Fed’s 2% target, reinforcing policymakers’ cautious tone. After the most aggressive tightening cycle in four decades, the Fed has effectively paused further rate hikes, and embarked on a cycle of rate cuts. So far the Fed has cut rates twice, while signaling it will move carefully toward additional rate cuts only if inflation continues to trend lower.

This environment—moderate growth, steady employment, and restrictive but stable policy—has proven more durable than many anticipated. Importantly, the economy is now demonstrating its ability to stand on its own, with growth supported by private investment and productivity gains rather than a reliance on monetary stimulus. That remains a sign of underlying strength, not fragility.

U.S. Stocks

Large-cap U.S. equities continue to anchor AMM’s core equity exposure. The fundamental backdrop remains solid: margins have stabilized, balance sheets are healthy, and productivity trends—driven by automation, reshoring, and AI adoption—are supporting earnings growth.

That said, valuations now reflect a great deal of optimism. The market’s forward P/E ratio remains above long-term averages, suggesting more modest returns from current levels. We expect returns to be increasingly driven by earnings growth rather than further multiple expansion. Encouragingly, market leadership has begun to broaden beyond the largest technology companies.

Source: FactSet, Standard & Poor’s, J.P. Morgan Asset Management

In our diversified asset allocation strategies, we continue to favor high-quality U.S. large-cap stocks—particularly dividend growers and companies with durable cash flows. We also maintain exposure to small- and mid-cap stocks, which have lagged in recent years but now trade at a meaningful discount relative to large caps.

While some of that discount is justified by the stronger fundamentals of larger companies, lower starting valuations can create fertile ground for future outperformance—especially if smaller firms are able to harness the power of AI and automation to boost productivity and profitability over time.

International Stocks

International markets have delivered very strong returns this year. Japan remains a standout, benefiting from improved corporate governance and shareholder returns. In contrast, Europe’s growth outlook remains subdued amid weak manufacturing and energy headwinds. China continues to face structural challenges from property-market imbalances and cautious consumers, but select emerging markets—such as India, Mexico, and parts of Latin America—are benefiting from supply-chain diversification and favorable demographics.

Valuations across international markets remain significantly lower than in the U.S., offering long-term opportunity for disciplined investors. However, near-term challenges—slower earnings growth, political uncertainty, and currency volatility—likely explain a good portion of the valuation discount. For this reason we continue to underweight International Stocks relative to their share of global market capitalization.

Fixed Income

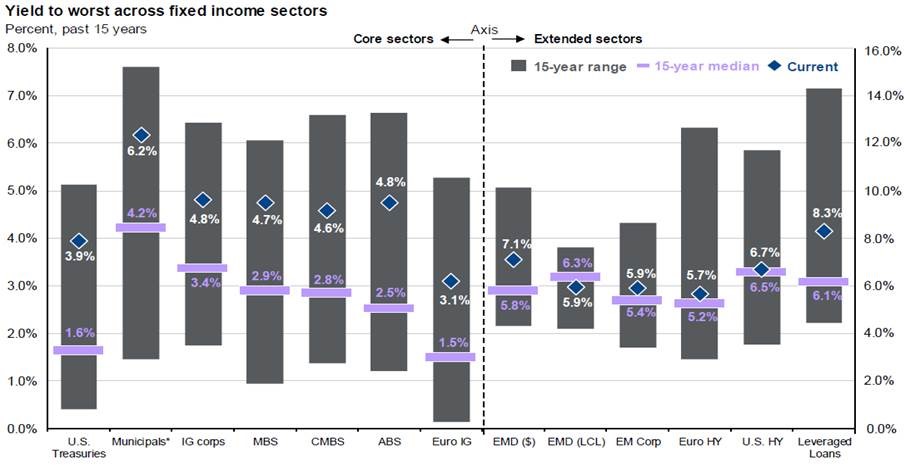

The running joke for many years, noted by James Grant of Grant’s Interest Rate Observer, was that bonds offered “return-free risk” instead of “risk-free return”. Following the bond market “reset” (i.e. bloodbath) of 2022, bonds now offer more meaningful income and real return potential. Yields remain near their highest levels since 2007, providing investors an opportunity to earn attractive income without taking excessive risk.

Source: Bloomberg, FactSet, J.P. Morgan Credit Research, J.P. Morgan Asset Management

In our fixed-income allocations, we continue to emphasize high-quality bonds with short- to intermediate-term durations—including U.S. Treasuries, investment-grade corporate debt, and mortgage backed securities. This diversified approach provides stability and flexibility should interest rates remain volatile.

We remain more cautious on lower-quality credit. Spreads on high-yield bonds remain tight relative to history, meaning investors are being compensated modestly for taking on default risk. As a result, we maintain limited exposure to high yield, favoring higher-quality issuers instead.

For qualified investors seeking additional yield and diversification, we continue to evaluate private income opportunities, including strategies backed by real assets or private credit with strong underwriting and conservative loan-to-value ratios. These investments can provide attractive yields and modest correlation to public markets, but we approach them selectively and with thorough due diligence given their liquidity constraints.

Conclusion

The market environment entering year-end 2025 may seem confounding. Earnings growth remains strong, yet valuations are elevated. Inflation has eased, but it’s still above the Fed’s 2% target. Consumer sentiment is cautious, even as spending remains resilient. And the geopolitical backdrop continues to offer both reasons for fear and grounds for hope.

Looking back through market history, none of this is unusual. Clear signals are a rarity in investing and in the economy. As cliché as it sounds, change really is the only constant in markets. The recession forecasts of 2022 and 2023 proved unfounded, replaced instead by optimism over a potential productivity-led economic boom. That theme has gathered momentum in recent years, but—like every trend before it—it will eventually evolve.

To navigate an ever-changing world, we will continue to anchor our decisions in our core principles: maintaining discipline on valuation, staying diversified across asset classes, and taking the long view that successful investing demands.

As always, we appreciate your continued trust and partnership, and we remain focused on helping you stay disciplined and invested through all phases of the market cycle.