As the year winds down, it’s a great time to review your tax, retirement, and legacy planning strategies. A few rule changes are in effect for 2025, and because timing matters, now is the moment to take a closer look. Below are several areas that deserve attention as you plan for the close of the year, followed by a quick reminder about Medicare open enrollment.

RMDs (Required Minimum Distributions)

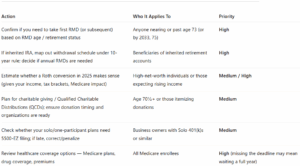

Thanks to SECURE 2.0, the age for beginning required minimum distributions has shifted. For those born between 1951 and 1959, RMDs must begin at age 73, while for those born in 1960 or later, the starting age is 75. The first RMD is due by April 1 of the year after you reach the required age, but delaying that first withdrawal means you’ll face two taxable distributions in one year (by April and again by December). All subsequent RMDs must be taken by 12/31 each year. While SECURE 2.0 reduced the penalty for missed RMDs, the costs are still steep enough to warrant careful planning. If you are at RMD age, we will reach out to you prior to year-end to make sure you distribute your RMDs for any accounts under our management.

Inherited RMDs / Inherited IRAs

If you’ve inherited a retirement account since 2020, be aware of the 10-year withdrawal rule. Confirm whether the IRA owner already took their RMD in the year of passing, if not, beneficiaries are required to distribute that amount to themselves prior to 12/31. After the year of death, in most cases, non-spouse beneficiaries must fully withdraw the account within 10 years of the original owner’s death. If the decedent had already begun taking RMDs, annual distributions are required in years 1 through 9, with the account fully depleted by the end of year 10. For inherited Roth IRAs, distributions are generally tax-free, but the same timing rules apply. These changes significantly reduce the ability to “stretch” an inherited account across a lifetime, so proactive tax planning is critical.

Charitable Giving & Qualified Charitable Distributions (QCDs)

For charitably minded retirees, Qualified Charitable Distributions remain a powerful tool. Individuals age 70½ or older can give directly from an IRA to a qualified charity and exclude up to $108,000 (2025 limit) from taxable income per individual. QCDs can also count toward RMDs, making them especially useful for those who want to reduce taxable income while supporting causes they care about. SECURE 2.0 also introduced a one-time option to give up to $54,000 via certain charitable remainder trusts or charitable gift annuities, opening another avenue for tax-efficient philanthropy.

Roth Conversions

Roth conversions are another strategic lever to consider before year-end. Converting funds from a traditional IRA or 401(k) into a Roth IRA means paying taxes now, but it allows for tax-free withdrawals later. This can be particularly valuable if you expect tax rates to rise in the future or your income to grow in retirement. Conversions should be weighed carefully, though, since they increase taxable income in the year of conversion and may affect Medicare premiums or other tax thresholds. If you have retired, and have not yet started receiving Social Security or RMDs, there may be an opportunity to do Roth conversions in these potentially lower income years. Please contact us if you would like to understand if Roth conversions make sense for you.

Action Items for Solo 401k Plans

Business owners with Solo 401(k)s or other one-participant plans need to be mindful of Form 5500-EZ filing requirements. If plan assets exceed $250,000 as of the end of the previous year, the filing is required. For calendar-year plans, the deadline for 2024 reporting was July 31, 2025, and electronic filing requirements now apply in many cases. If you missed the filing, consider correcting it promptly to minimize penalties.

For all solo 401k owners, you are also required to document your Employee contribution amount by 12/31. Actual contributions do not need to be made until your tax filing deadline (same as employer contributions). This is for your records only, you do not need to file anything with the IRS, but this record keeping is required and may be important if you were to be audited.

Other Year-End Planning Considerations

In addition to the items above, year-end is a good time to review your overall tax picture. Evaluate whether income or deductions should be accelerated or deferred, and consider strategies such as loss harvesting, maximizing business expense timing, or reviewing depreciation schedules. Even small shifts can make a big difference when it comes to your 2025 tax liability.

New Bonus Deduction for Seniors

For 2025, seniors can benefit from the Older Americans’ Bonus Benefit (OBBB) deduction, which provides an additional standard deduction of up to $6,000 each for taxpayers age 65 and older. This bonus deduction helps reduce taxable income beyond the regular standard deduction, offering extra relief to retirees and older filers. It’s important to note that the deduction phases out at higher income levels, so not all seniors will qualify. Be sure to review your adjusted gross income (AGI) against the phase-out thresholds to determine whether you’re eligible to claim the full benefit.

Medicare Open Enrollment

Finally, don’t forget Medicare’s annual open enrollment period, which runs from October 15 through December 7, 2025. During this window, Medicare beneficiaries can join, drop, or switch plans, including Part D drug coverage and Medicare Advantage. Since premiums, formularies, and provider networks often change, even those satisfied with their current coverage should review their options. Changes made during this period will take effect on January 1, 2026.

As always, please reach out to our office with any questions you may have.

Year-End Action Item Overview